Differentiating between hard savings and soft savings is one of the many responsibilities that fall to Procurement professionals. While the preferred method may vary from one organization to another, a standardized method of measuring savings is crucial to produce credible, meaningful results.

What Are Hard Cost “Savings”?

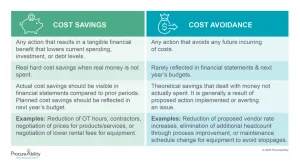

Definition: “Hard” cost savings can be described as tangible reductions that directly affect the company’s bottom line.

- Year over Year (YoY) savings achieved by purchasing in bulk

- Actions that directly affect the company’s bottom line

- Cost or asset reductions that directly happen as a result of process/technology/policy improvements

- Cost reductions of existing products or services, contractual agreements, or processes

- Cost reductions paid for items procured in comparison to prices paid for the prior 12 months

Examples Include:

- Reduced baseline – Reduction in resources based on targeted cuts

- Savings from budgeted spend

- Volume reductions – shrinking the amount of goods or services used

- Refunds/Rebates – Payments made by vendors as a result of increased spend or a savings project

What Are Soft Cost Savings / “Avoidance”?

Definition: “Soft” cost savings/avoidance can be described as actions that lower potential price increases so that a company does not have as many costs in the future.

- Does not lower the cost of products/services when compared against historical results, but mitigates the effect of cost increases

- Unpriced items offered as incentives by vendors

- Increased output/capacity without increasing resource expenditure, the soft cost savings are the amount that would have been spent to account for the increased volume/output, and

- Process improvements that positively impact efficiency, productivity, customer satisfaction, etc.; over time, the cost avoidance becomes cost savings.

Examples include:

- In-Contract cost avoidance – results from Procurement intervention(s) to mitigate price increases

- Free training, maintenance, or upgrades negotiated as part of the purchase

While there is a big focus on bottom line, hard savings, it is very common for Procurement teams to track both hard cost savings and cost avoidance. In order to effectively measure the value that Procurement brings to the table, there must be standardized methodologies that follow the organization’s values. Procurement should regularly meet with the Executive and Finance teams to align on the true value that Procurement is achieving through both streams. Interested in learning more about how best to present procurement information to executives?

Know When to Contact the Experts

Need help with assessing hard costs savings versus soft costs? Contact the experts at ProcureAbility today!

Subscribe to ProcureAbility Insights to access whitepapers, presentations, plus our latest thought leadership.